The smart part is where the money sits.

A PHSP cannot hold employee balances for years. So Zemma does something different: employers contribute into a trust, then Zemma uses insurance and a PHSP in a novel structure to release funds compliantly when it matters the most.

How the structure works

No more running out at the end of the year to max out on massages. The trust transfers funds to a person's PHSP on a reasonable schedule that better aligns with their health care needs.

Based on $300/mo over 3 years. Zemma can hold employer funds at the trust layer, then fund compliant PHSP reimbursements when claims happen.

Most of the market either pushes everything through insurance or pretends a PHSP can behave like a savings account. Zemma is different: we use a trust to hold employer money, insurance for risk, and a PHSP for compliant reimbursement.

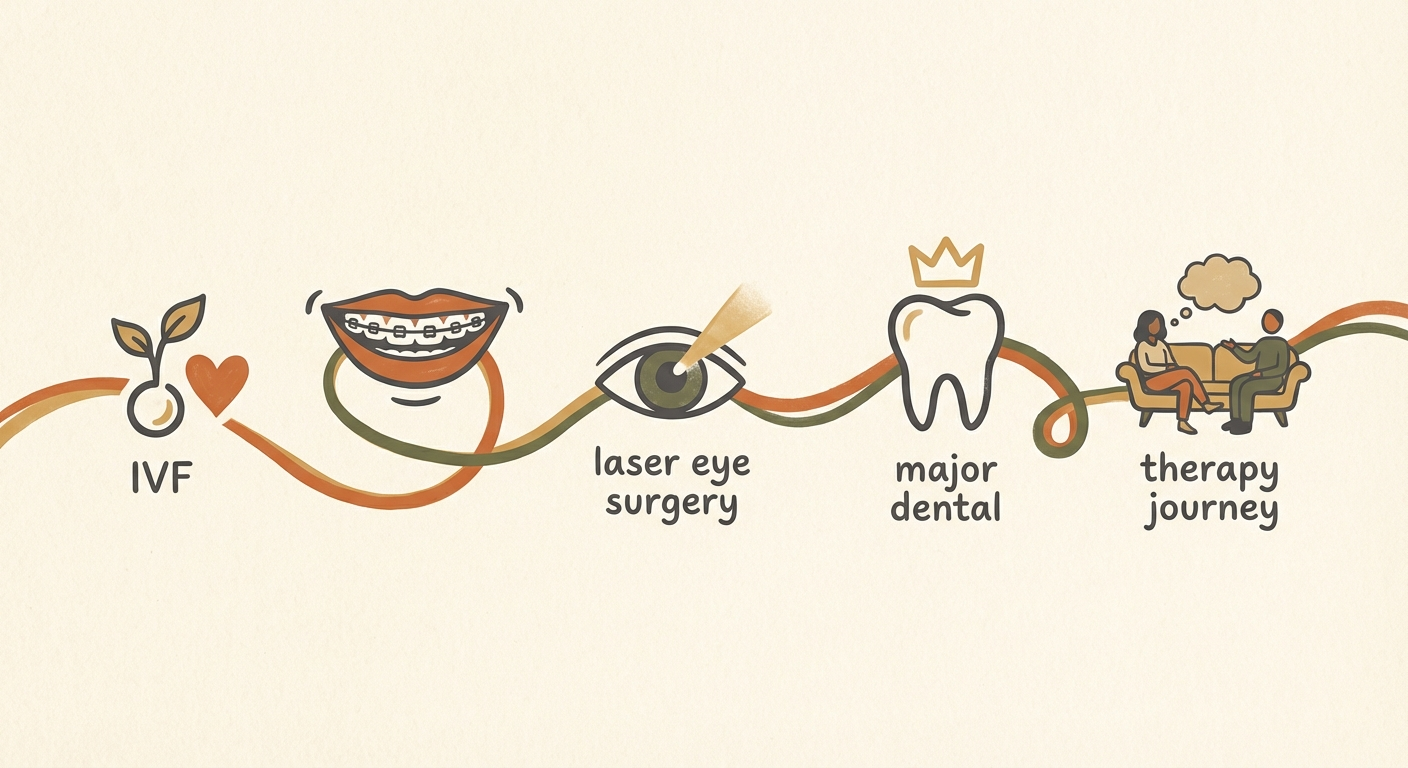

IVF treatments

Per cycle in Canada. CRA-eligible. One of the most significant healthcare expenses a family can face — and often requires multiple attempts.

Orthodontics / Braces

Full orthodontic treatment for children or adults. Traditional plans cap out fast. Zemma's trust structure gives employers a more practical way to fund real care over time.

Laser eye surgery

LASIK or PRK for both eyes. CRA-eligible. Most traditional plans don't cover it at all — it's almost never an "insured" benefit.

Major dental work

Implants, crowns, root canals, full restorations. Group dental limits get exhausted fast on serious work. These expenses arrive unpredictably.

Mental health / therapy

Real therapeutic work — regular sessions with a psychologist or therapist. Weekly care adds up fast and traditional plans cap out mid-year.

Mobility & specialist care

Custom orthotics, hearing aids, mobility devices, specialist consultations. Often CRA-eligible. Annual limits rarely match what people actually need.

Finally, a health account with the right layers.

The innovation is not pretending a PHSP can hold balances forever. The innovation is separating where employer money is held from how claims are ultimately paid.

The money goes into an employer health trust, not directly into a long-duration PHSP employee balance.

Catastrophic and insured events belong in insurance. That is still the right tool for unpredictable major risk.

When a member submits an eligible expense, the PHSP layer funds reimbursement within PHSP rules instead of being treated like a savings account.

Trust for holding employer money. Insurance for risk. PHSP for reimbursement. Most of the market only gives you one of those pieces.

Use it or lose it is a terrible product design.

Annual limits that expire force you to either scramble for receipts in November or lose money you earned. Neither outcome serves you.

Zemma lets you plan around your real life.

Deposits stay available for 7 years from the date they were made. You decide when to use them based on your actual health needs — not an arbitrary fiscal calendar.

Real healthcare doesn't happen on a fiscal calendar. Your health account shouldn't either.

Seven years from deposit. Yours until you need it.